Federal Reserve forecasting and watching

Warning, complex economics below (also see our intervention page)

On all charts, pay particular attention to the direction and trend of the rate of changes line(s).

Also, the Fed is not omnipotent and neither are we - the charts below are intended as guides and not guarantees.

Total borrowings from the Fed

Includes discount window, Term Auction Facility (TAF) and Primary Dealer Credit Facility (PDCF). Same as the Fed's monthly "BORROW" series, except weekly.

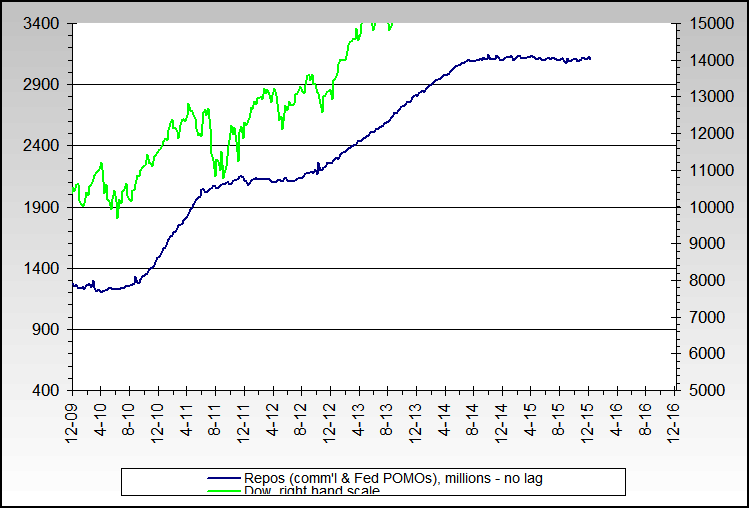

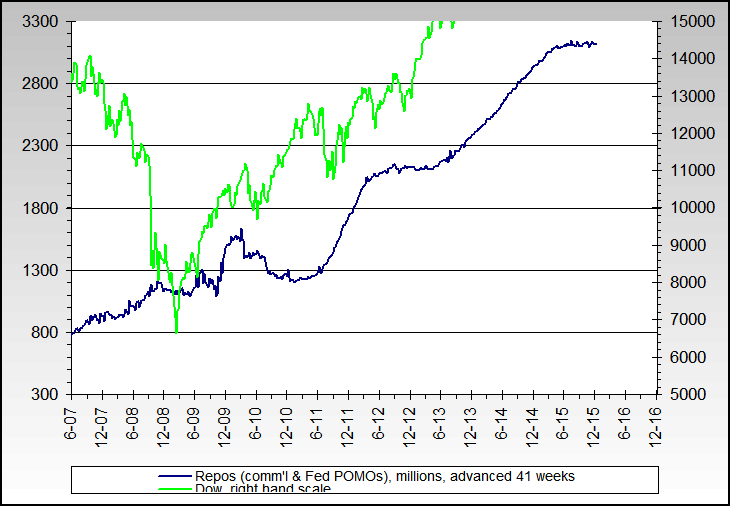

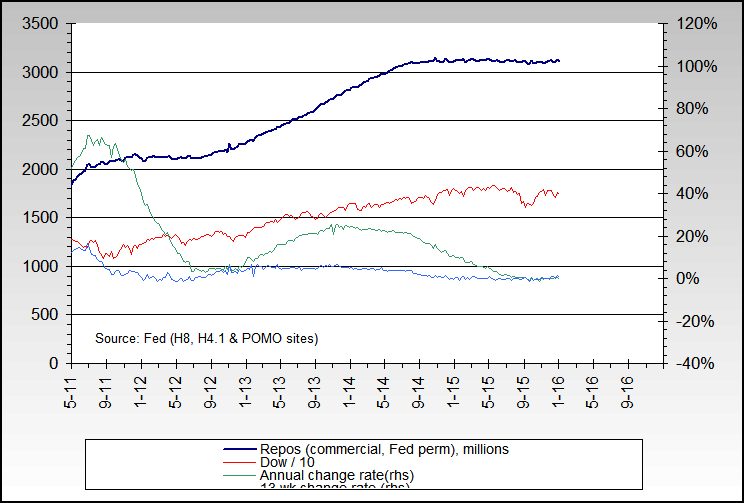

What does the Fed want the US stock markets to do?

The first chart shows repos and their almost immediate effects from changes in outstanding repo balances. The 2nd one assumes an approximate 41 week time lag until another effect is created on the Dow. The relationships have been fairly stable since 2002.

The 3rd one also shows how relatively fast or slow that repos are being created since its not always clear in the 1st one. Stock market support in late 2002 and early 2003 is particularly visible.

The basic theory behind its workability is that the large banks use the repo loans to buy & sell stocks.

Definition Source

Definition Source

Click here for the repo and Dow picture since 1980.

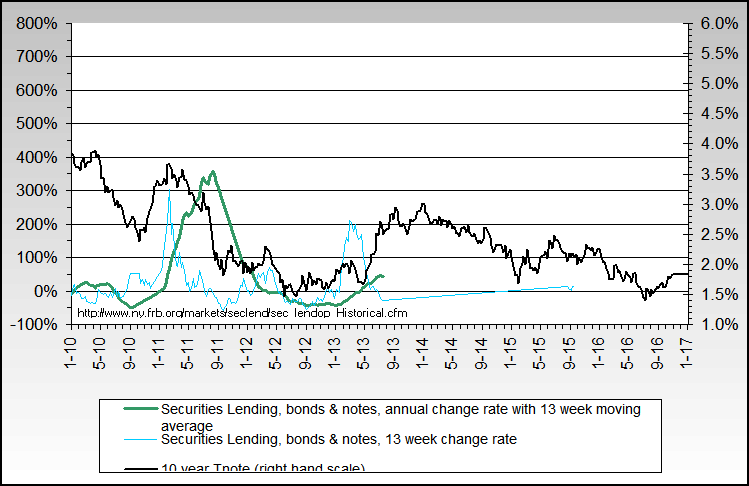

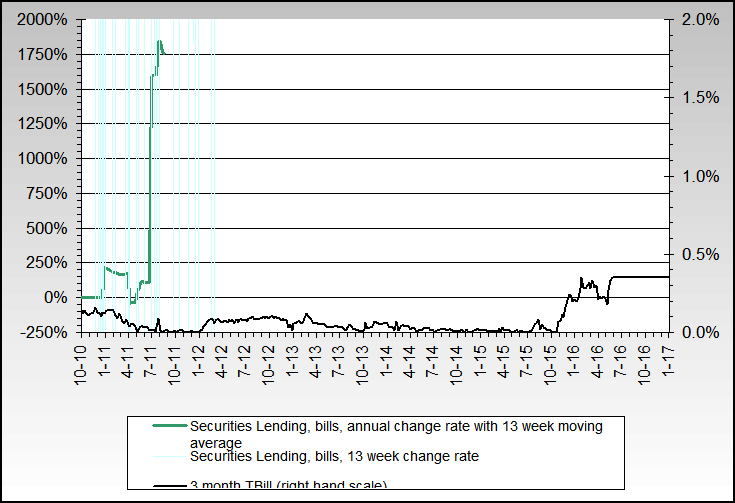

What does the Fed want to happen to interest rates?

There is a strong parallel or correlation between what interest rates do and how the rate of change of Securities Lending moves. Do note that during July-Sept 2006, interest rates did not do what the Fed seemed to desire. In other words, they don't always succeed in affecting interest rates.

Definition Source

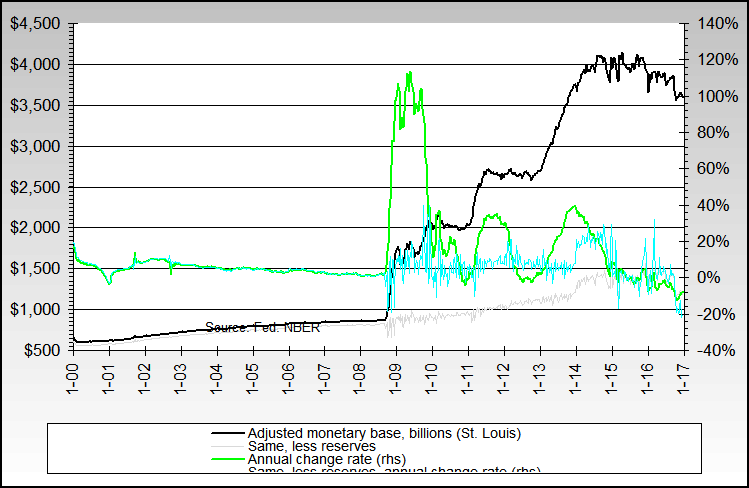

How much is the Fed concerned about U.S. inflation and/or deflation (and doing something about it)?

We see here that the Fed was concerned about inflation in 2000, moved to lower it, then likely judged they went too far and moved back up in 2001. There was also a large spike starting 9/11/2001.

Since then and up to early 2006, it has gradually been lowering the rate of money creation as measured by the monetary base.

Definition Source

Definition Source

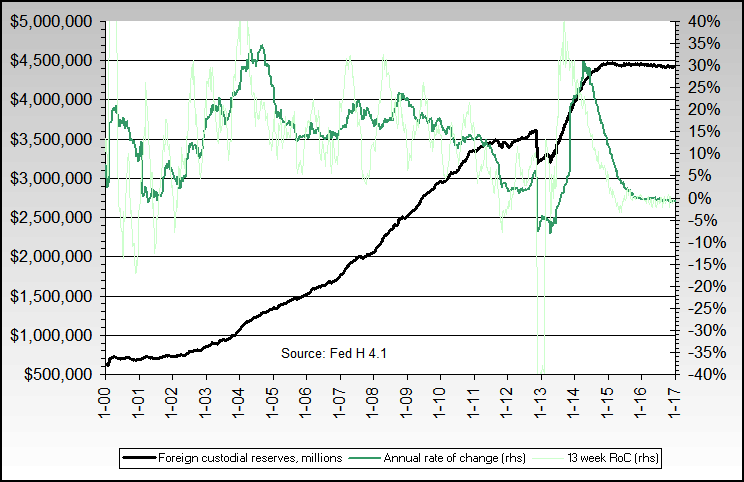

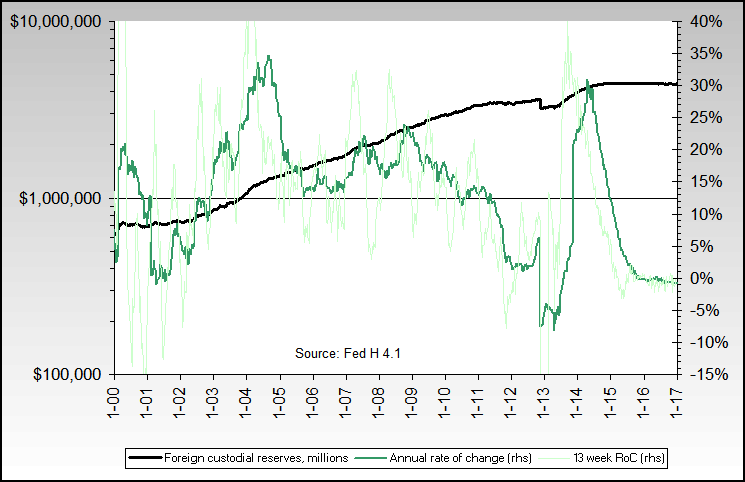

How strongly do other central banks feel about the US dollar?

How much are other central banks helping to monetize US debt?

Definition Source

Agencies only chart (chart above is total custodials)

T-Bills only chart

Starting in roughly August of 2004, the interest of foreign central banks in the US dollar as measured by custodials has been declining.

Here is another view of confidence of other central banks in the dollar It shows how much of their reserves are placed in dollars over the last few years, and their relative lack of confidence since 2002 and up to when this was written in early 2006.

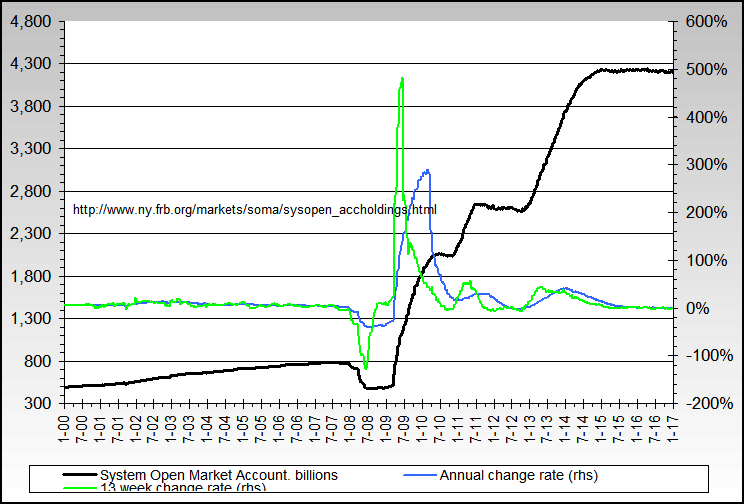

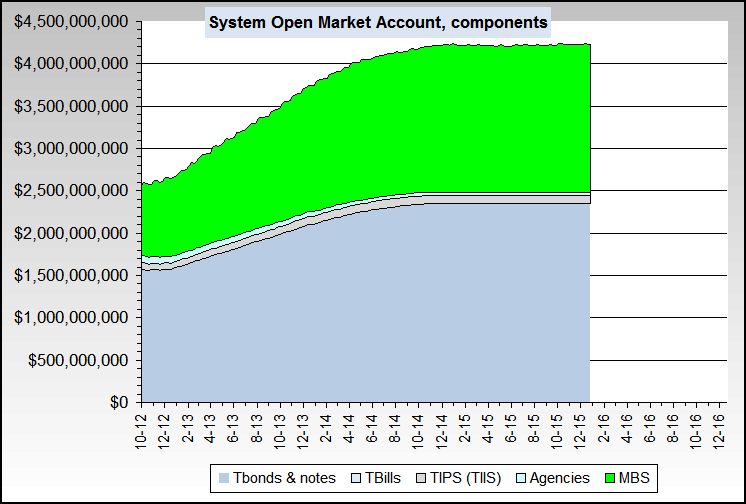

How much is the Fed supporting US Treasury Bonds and/or monetizing some of the debt?

Definition Source

Definition Source

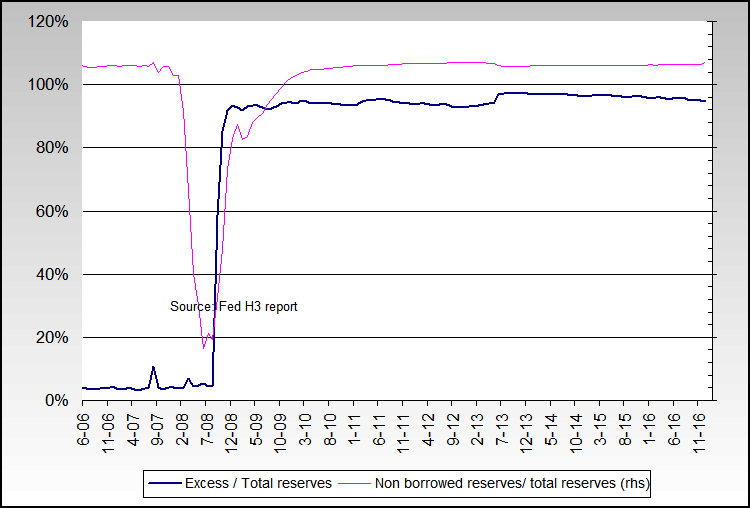

How easy is the Fed making money to borrow?

Definition Source 1 Source 2

Definition Source 1 Source 2

Notice that there has been plenty of reserves available at the banks for borrowing by the public during the entire period of the chart, regardless of the level of interest rates. Here's the same data going back to 1970.

Definition Source

Definition Source

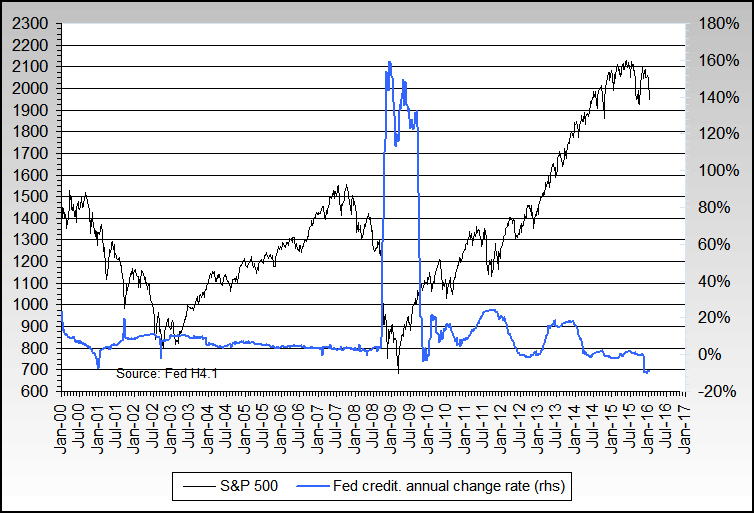

Notice that, as of mid 2006 and in spite of interest rates having gone up significantly, Fed credit is still growing at about a 5% rate and has sped up since late 2005. Also notice that large drops in Fed credit have a correlation, after a lag of a few months, with drops in the U.S. stock market.

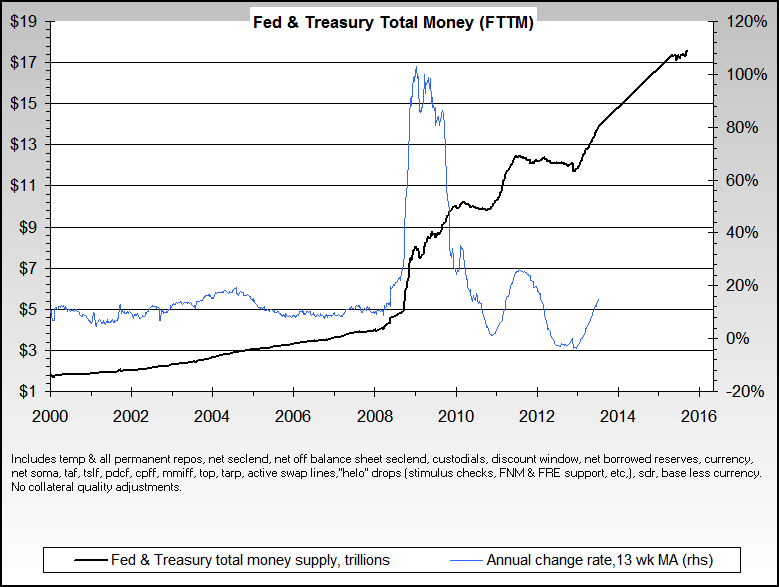

Fed total money supply

All major Fed operations (plus custodials), showing the running total of all Fed controlled money creation or destruction actions.

The red line shows the smoothed (via 13 week moving average) annual change rate of all Fed actions, and the black line adds in trading information of the Fed's primary dealers (GSDS). The blue line is the same as the red line, except is not smoothed with a 13 week moving average.

Please see the glossary for all definitions ("helo" drops defined as gov't tax rebates/stimulus checks)

Source for much of data

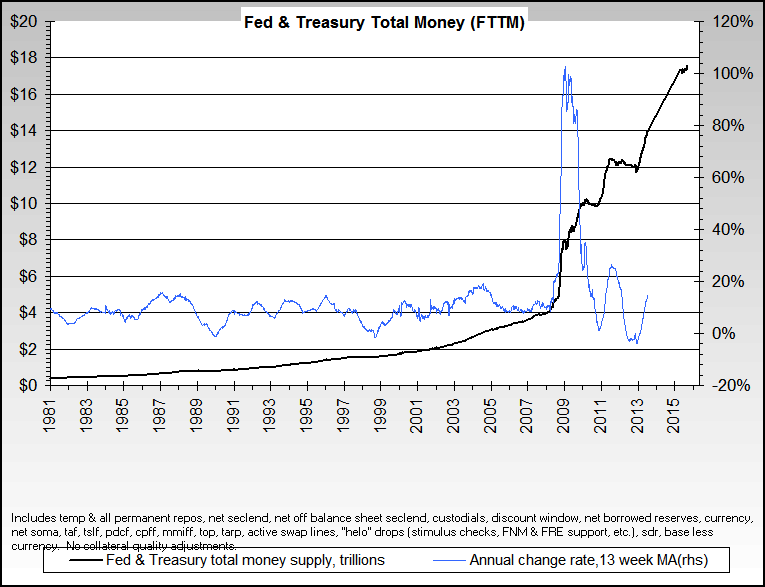

Same data, long term

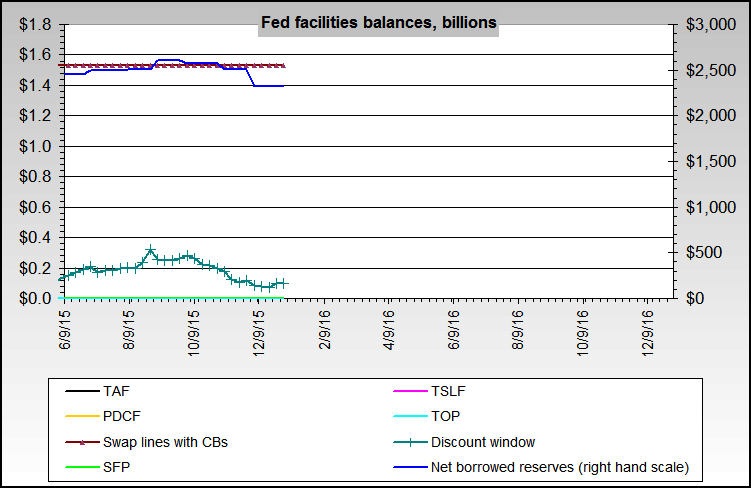

Facilities balances

Longer term

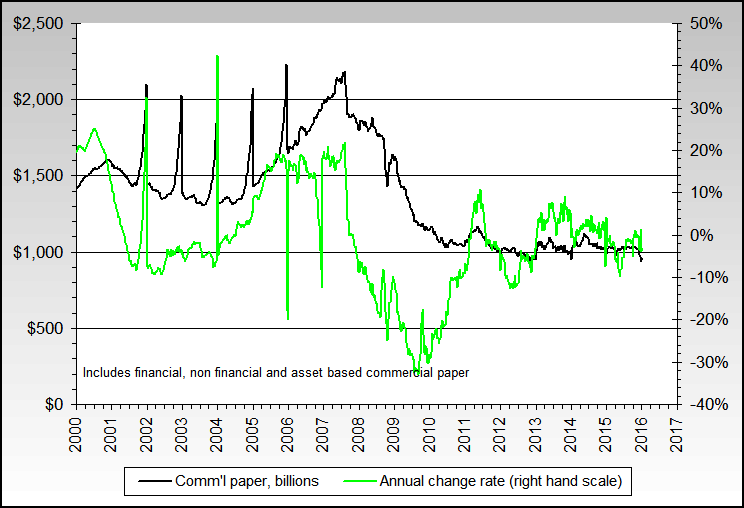

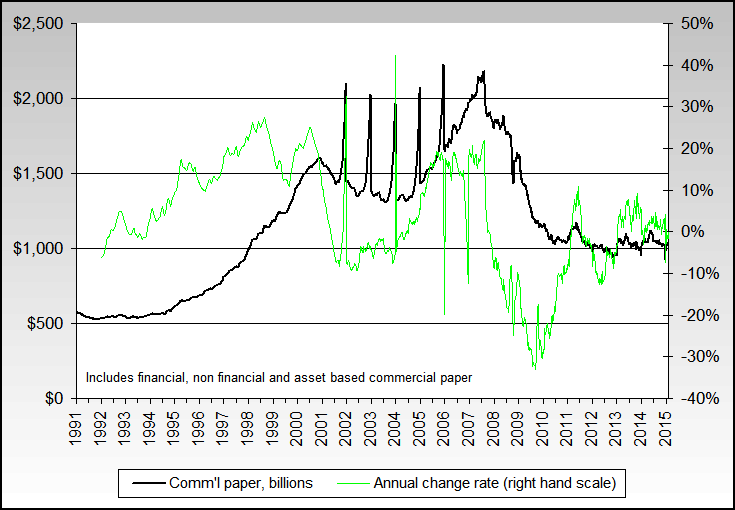

Commercial paper

Longer term

Components

Source

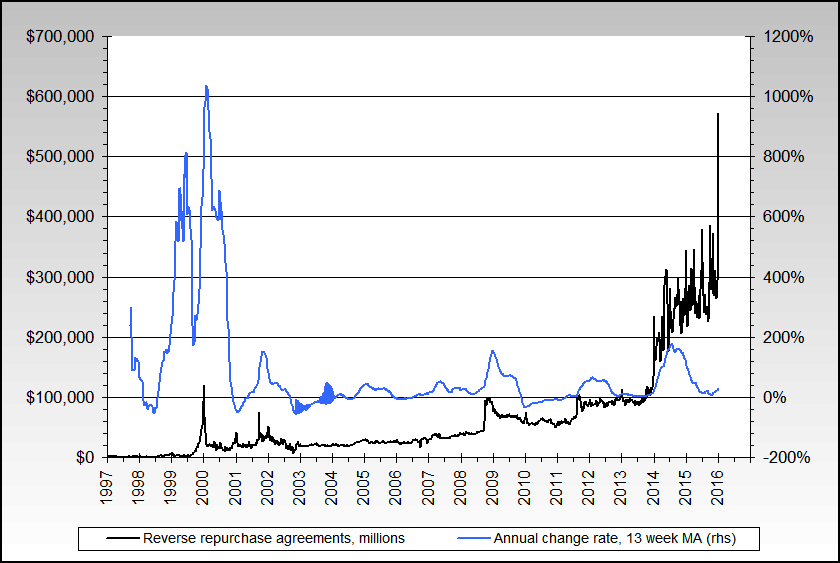

Reverse repos

How much is the Fed attempting to drain from money supply via reverse repos:

Source - H.4.1

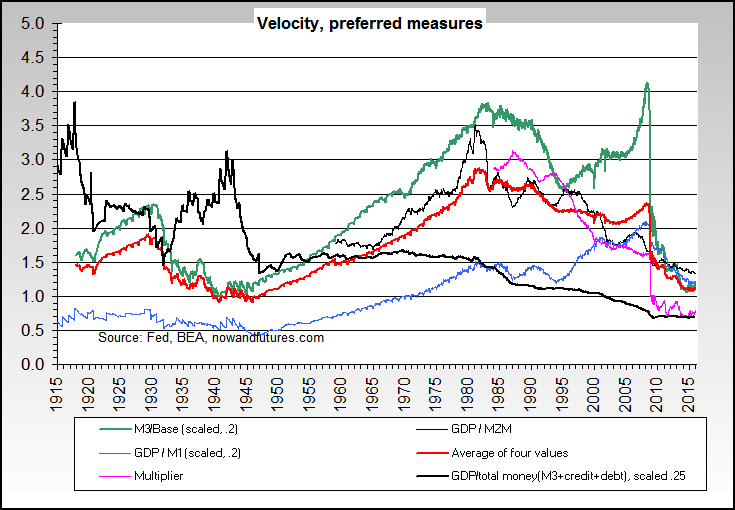

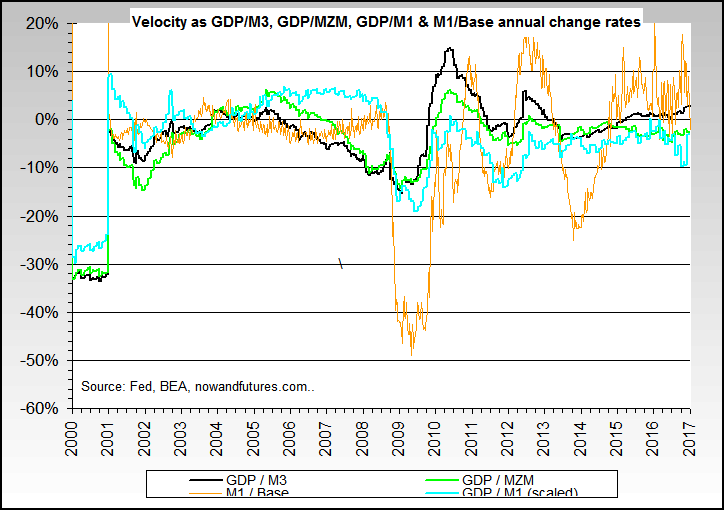

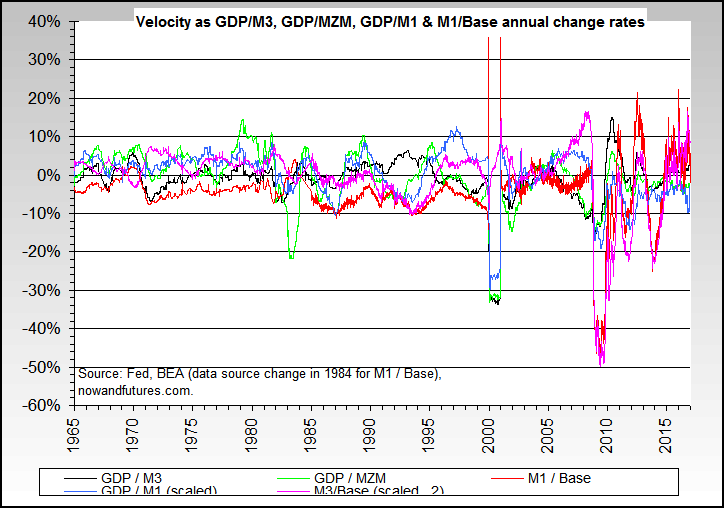

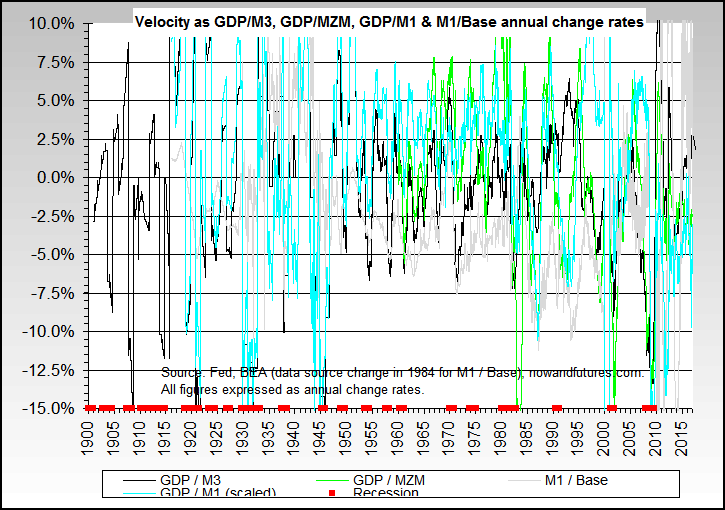

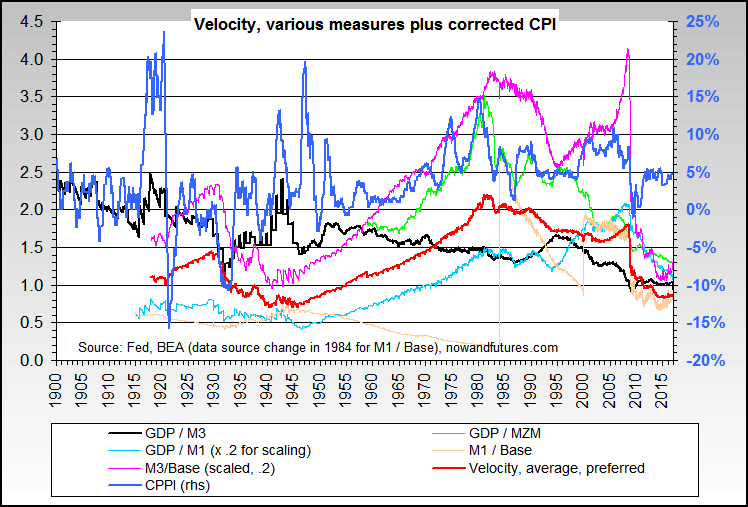

How fast is money moving through the U.S. economy?

The actual money of money and credit and debt being created is only part of the picture. Velocity must also be factored in since it affects the amount of total money in an economic system. Velocity is low in a depression and high in a hyperinflation.

Note that velocity is measured in many different ways, and that no single way is adequate to express it at all times. Note also that the bottom of a downward velocity trend does a decent but imperfect job of measuring the end of a recession or depression.

Long term

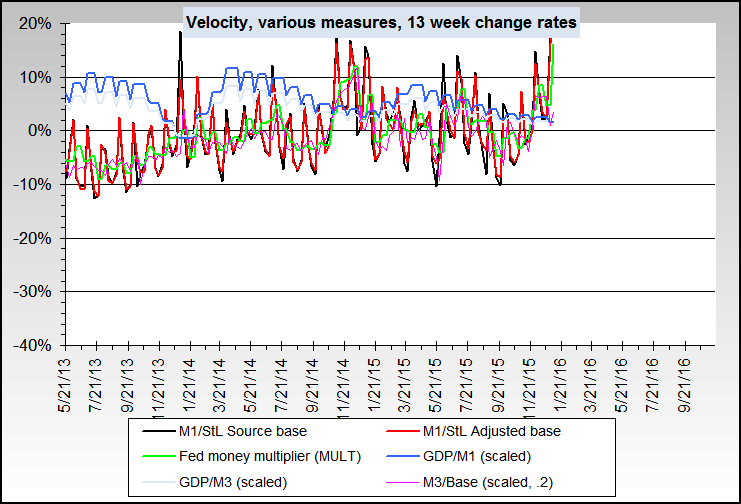

Short term

Definition Source: Fed & BEA

Definition Source: Fed & BEA

(Note: the huge jump in M1 / Base in 1984 was due to a definition change in base, and that it has been filtered out in the above chart)

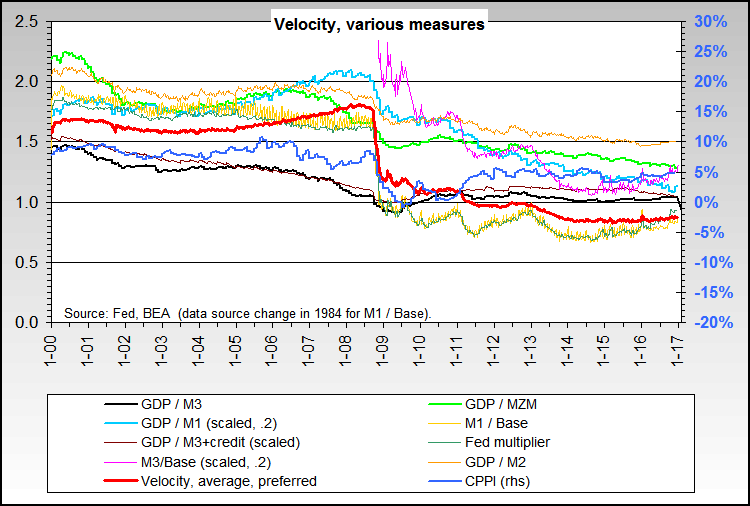

M2, M3 velocity

M1/Base velocity

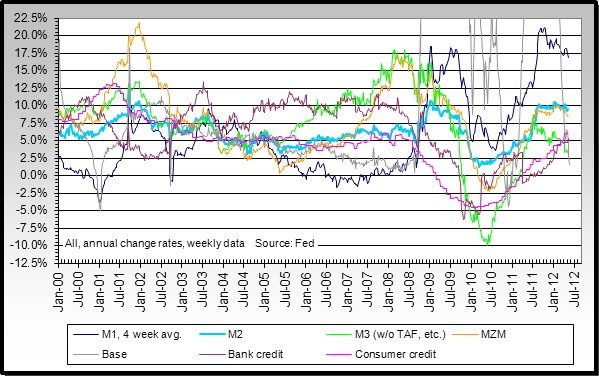

Various recent credit and money supply data, rates of changes

Definition Source

Definition Source

M1 vs. M1 plus sweeps, another change in definition issue that affects historical comparisons

Money supply, 1950-2005

Money supply, 1879-2006

Money supply, 1920-1940

Money supply, 1980-current

M3, MZM, base, credit, GDP, CPI since 1966 - (very wide chart)

Definition Source 1

Definition Source 1

Program trading, longer term

Program trading, long term

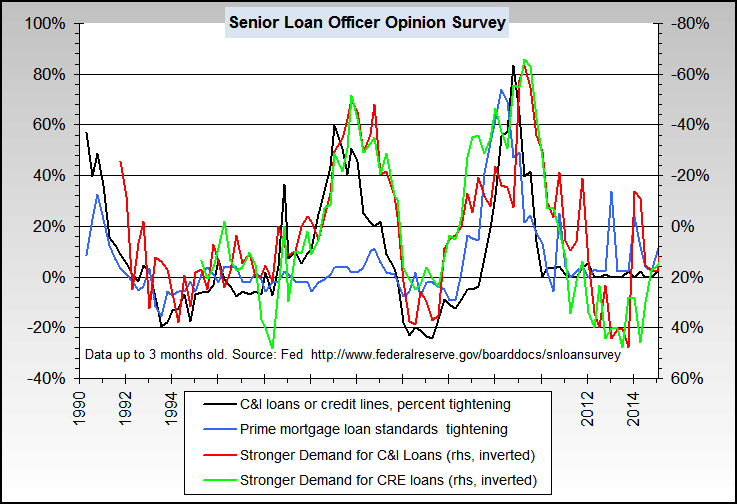

How easy are credit standards?

(Senior Loan Officer Survey) - source The Fed

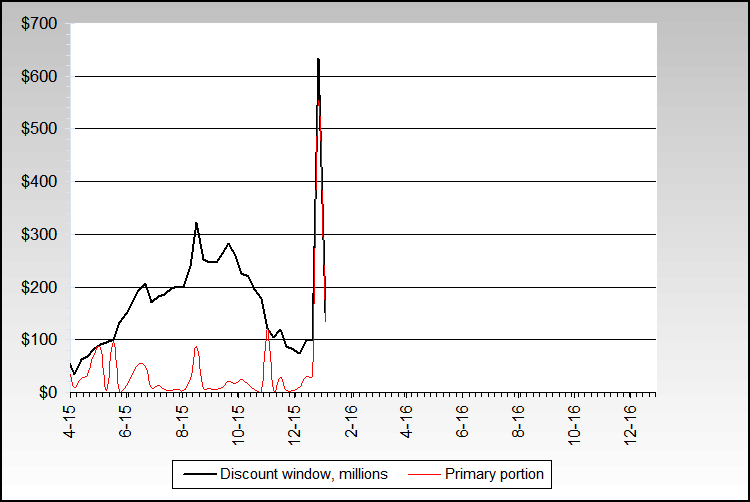

How much are banks borrowing from the Fed?

Click here for longer term chart

Here is the data on collateral accepted at the discount window.

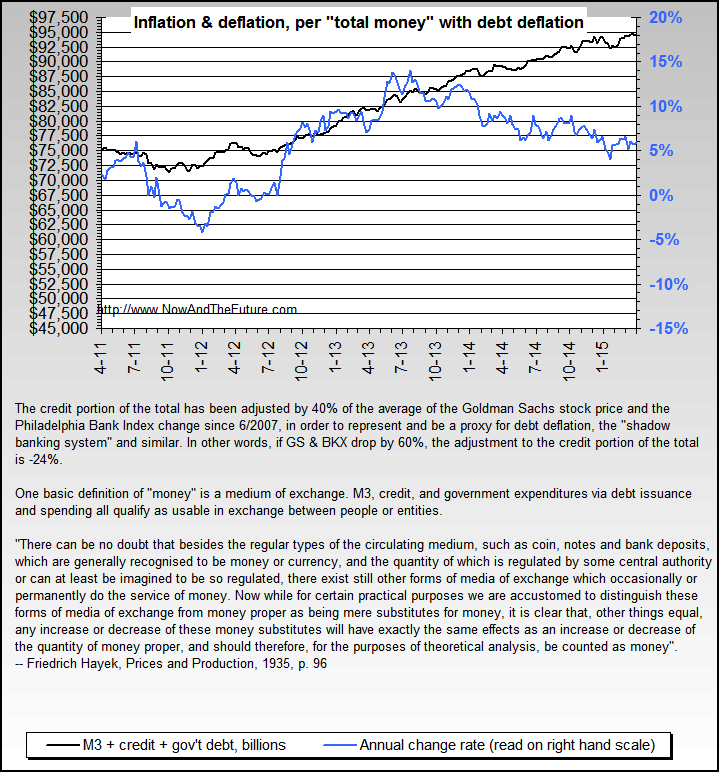

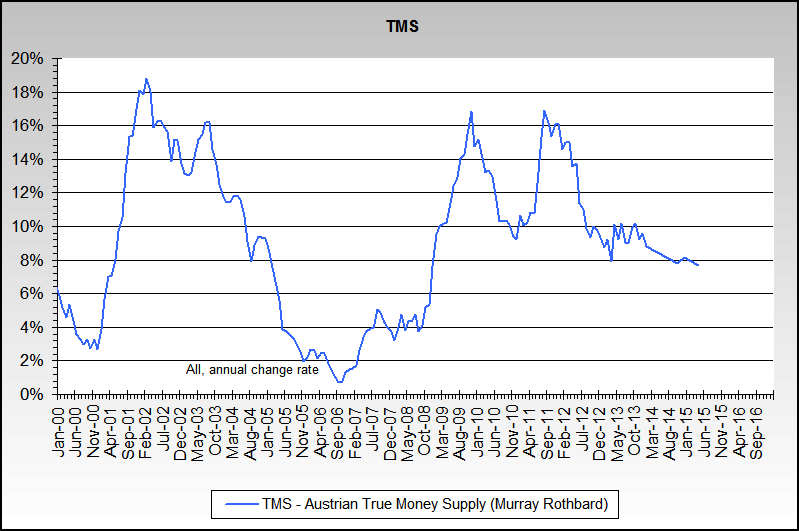

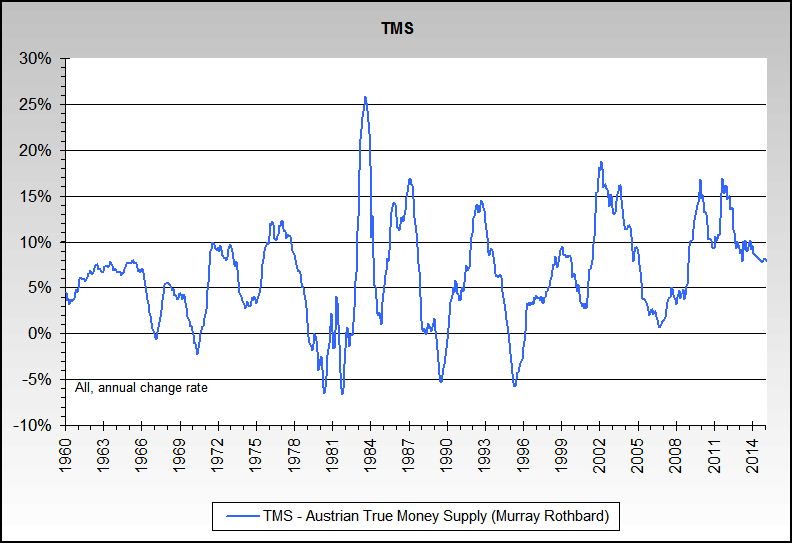

TMS - Austrian Money Supply

GSDS - Government Securities Dealer Statistics - total

GSDS - Government Securities Dealer Statistics - components

GSDS - Government Securities Dealer Statistics - component, changes rate

Definition Source

A historical perspection on the Federal Reserve's Monetary Aggregates: Definition, construction and targeting

Fed Chairman Ben Bernanke, etc. on Fed actions

"There is some evidence that central bank communications can help to shape public expectations of future policy actions and that asset purchases in large volume by a central bank would be able to affect the price or yield of the targeted asset."

Source: Monetary Policy Alternatives at the Zero Bound