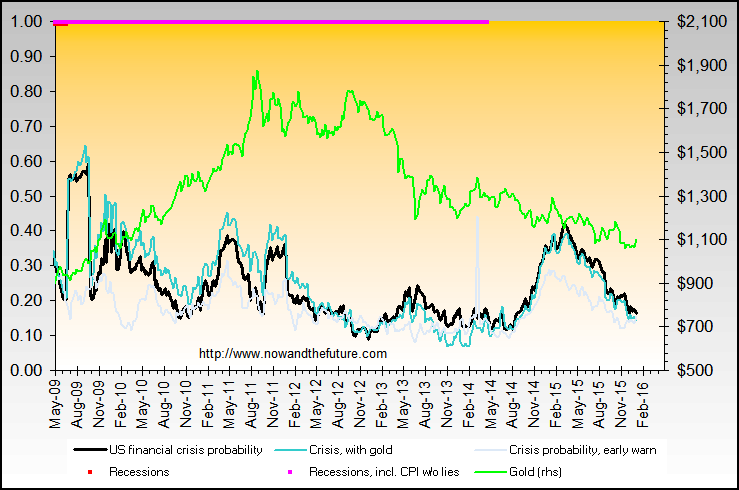

Leading indicators of a financial crisis |

|

|---|---|

| Leading indicator | Rationale |

| Current Account Real exchange rate Exports Imports Trade balance/GDP Current account balance/GDI |

Weak exports, excessive import growth, and currency overvaluation could lead to deteriorations in the current account, and historically have often been associated with currency crises in many countries. External weaknesses and currency overvaluation could also add to the vulnerability of the banking sector since a loss of competitiveness and the external market might lead to a recession, business failures, and a decline in the quality of loans. Banking crises could also lead to currency crises. |

| Capital Account Foreign reserves M2/foreign reserves Short-term debt/foreign reserves Foreign liabilities/foreign assets Deposits in BIS banks/foreign reserves |

With increasing globalization and financial integration, capital account problems could make a country highly vulnerable to shocks. Manifestations of capital account problems could include declining foreign reserves, excessive short-term foreign debt, debt maturity and currency mismatches, and capital flight. |

| Financial Sector M2 multiplier (M2/M0) Domestic credit/GDP Excess real M1 balances Central bank credit to public sector/GDP Domestic real interest rate Lending–deposit rate spread Real commercial bank deposits |

Currency and banking crises have been linked to rapid growth in credit fueled by excessive monetary expansion in many countries, while contractions in bank deposits, high domestic real interest rates, and large lending-deposit rate spreads often reflect distress and problems in the banking sector. |

| Real sector Industrial production Stock prices |

Recessions and a bust in asset price bubbles often precede banking and currency crises. |

| Global Economy US real interest rate US GDP growth World oil prices Dollar/yen real exchange rate |

Foreign recessions could spill over to domestic economies and lead to domestic recessions. High world oil prices pose a danger to the current account position, and also could lead to domestic recessions. High world interest rates often induce capital outflows. For many East Asian countries, the depreciation of the Japanese yen against the US dollar could put other regional currencies under pressure. |

| Fiscal Sector Fiscal balance/GDP |

Large fiscal deficits could lead to a worsening in the current account position, which could in turn put pressure on the exchange rate. |

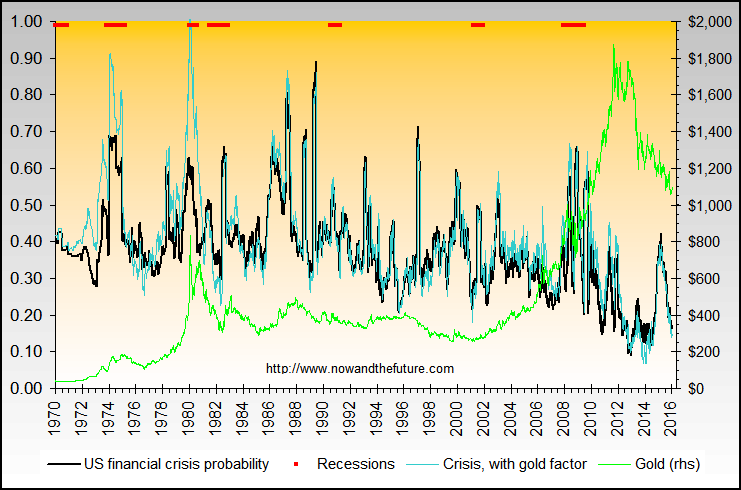

| Peak date | Event or issue | |

|---|---|---|

| Mid 1974 | OPEC oil crisis & recession | |

| Late 1979 | High inflation, gold over $800 | |

| Late 1982 | Deep recession | |

| Mid 1987 | International dollar valuation issues, stock market crash | |

| Late 1990 | International dollar valuation issues, Iraq war | |

| Early 1995 | International dollar valuation issues, high positive trade balance, oil price up about 60%, crisis in Mexico | |

| Early 1997 | Effects from Asian financial crisis | |

| Early 2000 | Stock market peak, oil price tripled since early 1999 | |

| Early 2003 | September 11 effects, oil price increases, dollar value loss |

Source of Leading Indicators from Asian Development Bank: Causes of the 1997 Asian Financial Crisis: What can an early warning system model tell us?

![]()